Pennsylvania RGGI CO2 Limits, Illinois Energy Bill, and CSAPR Update | Emissions Watch Blog

In this Emissions Watch blog, we provide updates on the Regional Greenhouse Gas Initiative (RGGI), an energy bill introduced in Illinois, the Ozone Season Cross-State Air Pollution Rule (CSAPR), and modifications to the federal Social Cost of Carbon.

RGGI Update

Relative to Q1 2020, Q1 2021 emissions in the Regional Greenhouse Gas Initiative (RGGI) footprint were 29 percent higher (excluding new members NJ and VA). The primary drivers of the elevated emissions were colder weather and higher natural gas prices. Heating Degree Days (HDDs) increased 9.1% in the RGGI footprint in Q1 year over year, and higher gas prices in February 2021 led to favorable economics for coal plant dispatch, thus increasing emissions.

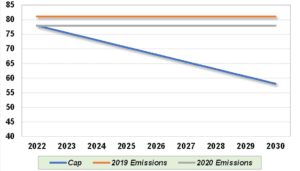

Notably, Pennsylvania released draft final regulations to join RGGI on May 4. The draft final regulations largely mirror those approved by the PA Environmental Quality Board (EQB) last September. The state would enter the RGGI program effective January 1, 2022, and the 2022 emissions limit would be set at 78 million tons and decline 3% each year through 2030. Figure 1 below shows the 2022 proposed cap against historical 2019 and 2020 emissions:

Figure 1: Proposed PA RGGI CO2 Limit vs. Historical 2019 and 2020 Emissions

One element of Pennsylvania’s draft final regulations that differs from those of other RGGI member states is a set-aside for waste coal facilities. This particular set-aside differs from the project-based set-asides in the 2017 RGGI Model Rule, which allows plant owners to use offsets from specified categories to satisfy up to 3.3% of their compliance obligations. The PA set-aside allocates emissions allowances directly to waste coal plants, and the total amount of set-aside allowances represents 13% of the total proposed 78 million ton statewide cap (10.4 million allowances). The set-aside effectively protects waste coal facilities from emissions compliance costs as long as their emissions remain below historical plant emissions.

Though mostly similar to last year’s approved proposed regulations, the draft final regulations include a provision to account for potential delays in joining RGGI due to strong opposition from PA Republican legislators. Instead of the proposed 78 million ton cap if the state joins on January 1, 2022, the cap would be 57.9 million tons if entrance occurs during Q1 2022, 40.7 million tons during Q2 2022 and 18.6 million tons during Q3 2022.

The inclusion of measures to address delayed entry underscores the significant opposition among state GOP officials to the adoption of an emissions cap. Republican state legislators introduced S.B. 119, which would require any emissions cap proposal to be brought before the state legislature. Additionally, state Republicans have told Democratic Governor Tom Wolf they will refrain from action on any appointments to the Public Utility Commission unless Wolf scraps plans to enact emissions regulations. Wolf indicated he would veto S.B. 119, and the state legislature does not have enough votes to override his veto.

ESAI believes it is likely the PA EQB approves final RGGI regulations later this year, but we also think it is likely the regulations get challenged in court on the grounds that the Governor did not have the authority to implement emissions regulations without legislative involvement. Additionally, Governor Wolf’s term expires in 2022, and his potential replacement by someone who does not support RGGI could alter the state’s current plans to join. ESAI will continue to monitor these developments.

Illinois Energy Bill

On April 29, 2021, the Illinois General Assembly introduced a comprehensive energy bill that could have significant ramifications on the state’s fossil generators and renewable energy development. The bill proposes achieving 100% “clean” energy by 2050, increasing the state’s RPS to reach 40% by 2030 and providing short-term subsidies to Exelon’s Byron and Dresden nuclear plants. Additionally, the bill proposes emissions caps and a carbon price that would affect IL fossil generators.

Fossil plants with units greater than 25 MW would be subject to declining emissions caps, reaching zero in 2030 for coal plants and in 2045 for gas and oil plants. The carbon price would start at $8/ton and escalate by 3% annually. The caps and carbon price would impact 51 fossil plants with a total generating capacity of over 29 GW. The state’s General Assembly has until May 31 to act on the bill, which is when its legislative session concludes. Regarding the nuclear subsidies, Exelon stated in early May that the proposed levels are insufficient to keep the Byron and Dresden plants open. ESAI is tracking this bill closely.

CSAPR Update

The EPA issued a revision to the federal Ozone Season Cross-State Air Pollution Rule (CSAPR) in March 2021 that reduces emissions caps for 12 states. The updated rule addresses provisions of the Clean Air Act that prohibit emissions in upwind states from causing nonattainment of National Ambient Air Quality Standards (NAAQS) in downwind states. The lower emissions caps apply to Louisiana, Virginia, West Virginia, Kentucky, Michigan, Illinois, Indiana, Ohio, Pennsylvania, Maryland, New Jersey and New York. The revised limits will be implemented through the new CSAPR NOx Ozone Season Group 3 Trading Program starting with this year’s ozone season (May through September).

Following the reduced ozone caps, allowance prices for vintage year 2021 were trading at $3,000/allowance in early March before declining to $2,675/allowance (as of May 21), levels that both far exceed prices for 2019 and 2020 that averaged $188/allowance. However, ESAI believes allowance prices are high relative to the current supply of allowances and will continue to fall. ESAI will provide an updated Ozone Season CSAPR allowance forecast in the June 2021 Energy WatchTM Quarterly.

Social Cost of Carbon Update

In January, President Biden issued Executive Order 13990, which re-established the Interagency Working Group on the Social Cost of Greenhouse Gases (IWG) to update metrics that assign monetary value to the impacts of emissions: the Social Cost of Carbon, Social Cost of Nitrous Oxide, and Social Cost of Methane. In February 2021, the IWG established interim values for these metrics while it works to calculate new finalized values. The interim value for the Social Cost of Carbon (SC-CO2) is $51/metric ton, which is much higher than the $1-$7/metric ton value established during the Trump Administration. Increases to the SC-CO2 will impact state and federal-level cost-benefit analyses, and higher levels will provide greater justification for policies that help achieve the Biden administration’s ambitious zero-carbon goal for the power sector by 2035. The IWG is working to update the values, and ESAI will provide an update on this progress.

More Information

Look for the launch of our Renewable Energy service launching in Q3. For more information and specific price data, check out ESAI’s Free Trial Service.

Learn About Emissions Watch

This quarterly publication contains ESAI Power’s outlooks and views on the emissions markets. ESAI provides regular updates and analysis on developments in the SO2, NOx and CO2 emissions markets as well as price forecasts for state and regional markets. In addition, regular updates are provided on the RGGI program as well as other state-specific emissions programs.

Learn About Energy Watch Quarterly

Energy Watch QuarterlyTM provides a quarterly analysis of market and policy issues affecting energy pricing dynamics over the next 10-year period for both the power and natural gas sectors. This analysis includes forecasts of pool-wide and zonal energy prices in New England, New York, and PJM, including forecasts of fuel inputs. Supporting assumptions are provided in each quarterly report.